Featured Snippet:

High net worth financial planning in 2026 is no longer just about growing wealth, it is about protecting it. AI-driven markets, rising fraud risk, and shifting tax law have made preservation the new priority. Sid Bindra, CFP® and founder of The Bindra Group (LPL/Linsco), named to Forbes’ Top Next-Gen Wealth Advisors Best-In-State list, shares with his close personal friend, Bob Generale of Percepture, to ensure HNW families are found, trusted, and protected, in AI search and in real life.

Video: “High Net Worth Financial Planning in 2026: Preservation Beats Hype | Sid Bindra CFP®”

‘

Caption: “Sid Bindra explains why 2026 rewards discipline in wealth management and financial planning.”

Transcript

High Net Worth Financial Planning in 2026: Preservation

[00:00]

Wealth management this year is really more about preservation. I believe preservation is the word most wealth managers should be focused on in 2026.

[00:16]

The fundamental changes in society are going to evaporate quite a bit of the wealth that’s been created over the last six years.

[00:28]

Since COVID, we had two years of the money printer. Then inflation came with a vengeance. As we transition into 2026, what you did during the pandemic really propels you into the next part of your career. For me personally, my life and career moved forward because I didn’t fall apart during the pandemic.

[00:54]

But we are going to be paying the bill of the pandemic. We have not been paying that bill. It has continued to grow.

[01:03]

The deficit continues to grow. Government policy is not moving in the direction of reducing the bill. It keeps getting bigger and bigger.

[01:12]

The interest on that bill is also growing, and it’s becoming a larger part of GDP. That is essentially an evaporation of wealth.

[01:22]

So in 2026, if you’re not seeing that — if you’re still looking at life through rose-colored glasses — there’s a reality check you need to be aware of.

[01:35]

The opportunities in wealth management are fairly clear. Energy is the top theme. It’s the biggest theme we all need to be paying attention to, and it will likely remain a dominant theme for years.

[01:57]

In wealth management, there’s value versus growth. Growth has been the primary driver of stock market returns since 2008 — really since quantitative easing began and lower interest rates became the norm.

[02:08]

That era effectively ended in 2022. Quantitative easing stopped. Interest rates increased. Money became tighter.

[02:21]

For growth to meaningfully outperform again, there would likely need to be some return of quantitative easing.

[02:31]

In the meantime, you need to focus on fundamentals. My biggest advice from an outlook perspective is to become a boring investor.

[02:43]

Look at what happened in gold and silver over the last year. That should be a major indicator of what’s to come.

[02:51]

The last time gold spiked like this was in 2006, 2007, and 2008. We all remember what happened in 2008.

[02:59]

It’s a telling sign. Governments are hoarding precious metals. Prices are rising. That signals preparation for something.

[03:11]

If governments are preparing and hedge funds are positioning themselves, investors cannot afford to remain reactive. This is where the difference between passive and active investing becomes important.

[03:26]

We need to change our mindset and become more actively involved. 2026 is about preparing for a storm.

[03:35]

The storm is coming. It’s here. We need to put the shutters in place, batten down the hatches, and prepare for a battle.

[03:45]

Prepare for the worst. Hope for the best.

[03:51]

That’s the mentality you need in 2026. If you don’t have that mindset, the wealth you gained over the last decade is at risk.

[03:59]

And that is not how you protect wealth.

What is high net worth financial planning?

High net worth financial planning is a structured approach to managing, protecting, and transferring wealth for individuals and families with $1 million or more in investable assets.

It is different from standard financial planning. The stakes are higher. The tax exposure is larger. The estate complexity is real. And the risks — from market swings to fraud — hit harder when more is on the line.

Financial planning for high net worth individuals covers a wide range of needs:

- Investment strategy built around preservation, not just growth

- Tax planning that reduces what you owe — legally and proactively

- Estate planning that protects your legacy across generations

- Risk management that accounts for modern threats like deepfakes and identity fraud

If you have built significant wealth, a general financial plan is not enough. You need a plan built for your level of complexity.

Who it is for:

- Families with $1M–$30M+ in investable assets

- Business owners approaching a liquidity event

- Executives with concentrated stock positions

- Retirees managing multi-decade drawdown strategies

Need Financial Planning Advice

High net worth preservation requires more than a standard portfolio. It requires a coordinated strategy between institutional wealth management and digital security. Schedule a private consultation with Sid Bindra to audit your preservation plan.

Why 2026 is a “preservation year”

Sid Bindra puts it plainly: “This is a year to batten down the hatches.”

After more than a decade of low rates and easy growth, the environment has shifted. Volatility is back. Tax law is uncertain. AI is changing how markets move and how fraud is committed. HNW families who built wealth in the growth era now face a different challenge: keeping it.

5 signals HNW families are watching in 2026:

- Tax law uncertainty — Key provisions from the 2017 Tax Cuts and Jobs Act are set to expire. Estate and gift tax exemptions may drop significantly.

- AI-driven market volatility — Algorithmic trading and AI-generated news cycles are creating faster, sharper market swings.

- Rising fraud risk — Deepfake audio and video are being used to impersonate advisors and family members. Identity theft targeting HNW individuals is at an all-time high.

- Generational wealth transfer — An estimated $84 trillion will transfer between generations over the next 20 years (Cerulli Associates). Planning now matters.

- Interest rate complexity — Higher-for-longer rates are reshaping fixed income, real estate, and alternative investment strategies.

Chart: “2008–2022 vs 2026: Growth Era vs Preservation Era”

| Era | Primary Goal | Key Risk | Strategy |

|---|---|---|---|

| 2008–2022 | Maximize growth | Missing the rally | Aggressive allocation |

| 2026 | Preserve & protect | Volatility + fraud + tax | Disciplined preservation |

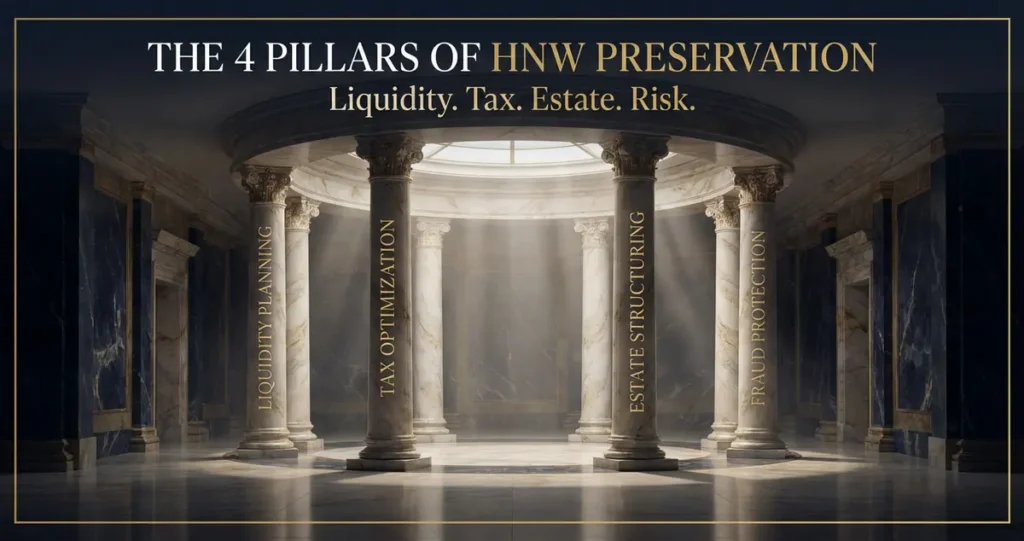

The 4 pillars of high net worth financial planning

A strong plan for HNW families is built on four pillars. Each one matters. Together, they form a system.

Pillar 1: Liquidity Planning

You need cash when you need it — not after a forced sale. Liquidity planning ensures HNW families can meet short-term needs without disrupting long-term strategy. This means holding the right amount in accessible, low-risk vehicles while keeping the rest working harder.

Pillar 2: Tax Planning for High Net Worth Individuals

Tax planning for high net worth individuals is one of the highest-leverage activities in wealth management. Done well, it can save hundreds of thousands of dollars per year. This includes Roth conversion strategies, tax-loss harvesting, charitable giving structures (DAFs, CRTs), and business entity optimization.

Pillar 3: High Net Worth Estate Planning

High net worth estate planning is about more than writing a will. It is about structuring trusts, gifting strategies, and beneficiary designations so your wealth transfers the way you intend — with minimal tax drag and maximum clarity. With exemptions potentially dropping in 2026, acting now is critical.

Pillar 4: Risk + Fraud Protection

Retirement planning for high net worth individuals must now include a layer most advisors overlook: fraud and identity protection. Deepfake technology can replicate a voice or face in seconds. HNW families are prime targets. A modern plan includes:

- Multi-factor authentication on all financial accounts

- A documented “voice verification” protocol with your advisor

- Regular dark web monitoring

- Clear process for wire transfer approvals

The 4 Pillars at a Glance:

- ✅ Liquidity Planning

- ✅ Tax Planning for High Net Worth Individuals

- ✅ High Net Worth Estate Planning

- ✅ Risk + Fraud Protection

🔒 Own topics in AI Search.

Leverage the same ‘Chatham House’ level of security and institutional strategy used by the world’s leading digital infrastructure CEOs. Condition markets and investor relations with AI Search strategy

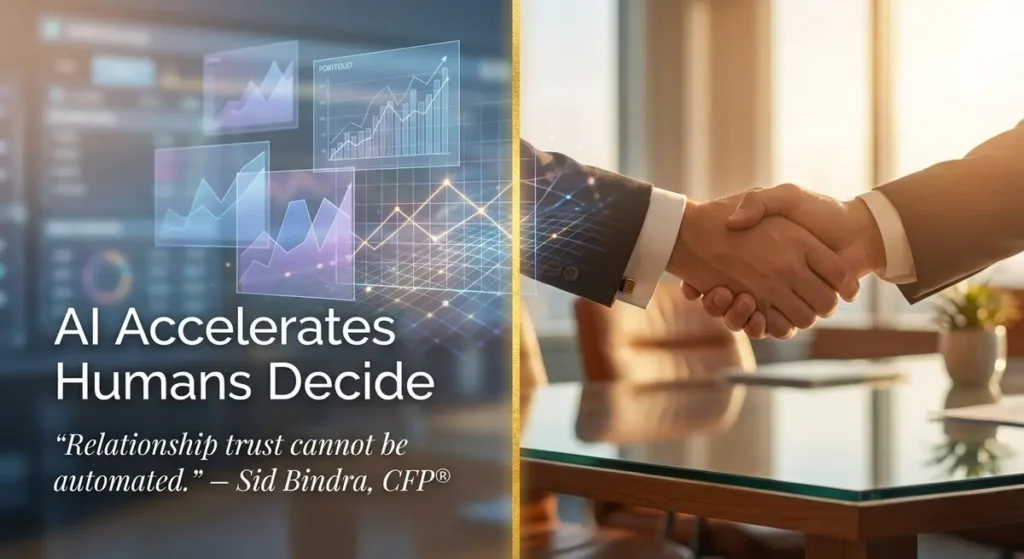

Where AI helps — and where people must lead

AI is changing high net worth financial planning. That is not a warning. It is a fact.

AI tools can scan thousands of data points in seconds. They can flag tax inefficiencies, model estate scenarios, and monitor portfolios around the clock. For HNW families, this is a real advantage.

But AI cannot do everything.

Sid Bindra is direct about this: “Relationship trust cannot be automated.”

When a client calls at 11 pm because markets are moving and they are scared, that is not a data problem. It is a human moment. When a family is deciding how to structure a trust for a child with special needs, it requires judgment, empathy, and accountability. No algorithm carries that weight.

The best high net worth financial planning in 2026 uses AI for speed and pattern recognition. It uses humans for responsibility, judgment, and client reality.

Where AI helps:

- Portfolio monitoring and rebalancing alerts

- Tax-loss harvesting triggers

- Fraud pattern detection

- Document processing and compliance checks

Where humans must lead:

- Client relationship and trust

- Complex estate decisions

- Behavioral coaching during volatility

- Ethical judgment calls

Learn how Percepture builds AI-search authority for regulated industries →

A simple checklist HNW families can use this week

You do not need to overhaul your entire plan today. Start here.

- Review your estate documents. Are your wills, trusts, and beneficiary designations current?

- Check your tax exposure. Has your advisor modeled the impact of expiring TCJA provisions on your estate?

- Audit your liquidity. Do you have 12–24 months of living expenses in accessible, low-risk accounts?

- Verify your fraud protection. Do you have a voice verification protocol with your advisor?

- Review your insurance. Does your umbrella policy reflect your current net worth?

- Check your charitable giving structure. Are you using a DAF or CRT to reduce taxable income?

- Confirm your advisor’s credentials. Are they a CFP®? Are they a fiduciary?

- Review your investment allocation. Does it reflect a preservation-first posture for 2026?

- Check your digital security. Are all financial accounts using multi-factor authentication?

- Schedule a full plan review. When did you last do a comprehensive review with your advisor?

2026 Wealth Preservation Check

Answer these 5 questions to see where your plan stands.

1. Do you have a current estate plan reviewed in the last 2 years?

- Yes / [ ] No / [ ] Not sure

2. Has your advisor modeled the impact of expiring tax exemptions on your estate?

- Yes / [ ] No / [ ] Not sure

3. Do you have a documented fraud/identity protection protocol with your advisor?

- Yes / [ ] No / [ ] Not sure

4. Is your investment allocation aligned with a preservation-first strategy for 2026?

- Yes / [ ] No / [ ] Not sure

5. Have you reviewed your beneficiary designations in the last 12 months?

- Yes / [ ] No / [ ] Not sure

⚠️ Educational only. Not financial advice. Consult a licensed CFP® or fiduciary advisor before making any financial decisions.

How to choose a wealth manager for high net worth financial planning

Not every advisor is built for HNW complexity. Here is what to look for.

Credentials:

- CFP® (Certified Financial Planner) — the gold standard for comprehensive planning

- CPA or CPA/PFS — critical if tax planning is a priority

- CPWA® or CIMA® — specialized for high net worth and ultra-HNW clients

Process:

- Do they have a documented planning process?

- Do they use a team model or a solo advisor model?

- How do they handle estate and tax coordination with your other advisors?

Identity + Security:

- How do they verify your identity before executing transactions?

- Do they have a documented wire transfer approval process?

- How do they protect your data?

Documentation:

- Do they provide written financial plans — not just investment statements?

- How do they document decisions and recommendations?

- Are they a fiduciary — legally required to act in your interest?

How to build digital trust?

In 2026, being an expert isn’t enough—you have to be the verified answer in AI search. Percepture specializes in positioning HNW advisors and tech leaders as the dominant authorities in their field through high-stakes Digital PR and Generative Engine Optimization.

FAQ: High Net Worth Financial Planning in 2026

What is high net worth financial planning?

High net worth financial planning is a comprehensive approach to managing wealth for individuals with $1M+ in investable assets. It covers investment strategy, tax planning, estate planning, and risk protection — all coordinated to preserve and grow wealth across generations.

Who needs high net worth financial planning?

Anyone with $1 million or more in investable assets benefits from HNW-specific planning. This includes business owners, executives, retirees, and families managing inherited wealth. The complexity of tax, estate, and risk management at this level requires specialized expertise.

What is the difference between financial planning for high net worth individuals and standard planning?

Standard planning focuses on budgeting, saving, and basic investing. Financial planning for high net worth individuals adds layers: tax optimization, trust structures, estate planning, alternative investments, and fraud protection. The stakes — and the strategies — are fundamentally different.

How does AI affect high net worth financial planning in 2026?

AI helps advisors monitor portfolios, flag tax opportunities, and detect fraud patterns faster than ever. But AI cannot replace human judgment in complex estate decisions, behavioral coaching, or relationship trust. The best advisors use AI as a tool — not a replacement.

What is high net worth estate planning?

High net worth estate planning is the process of structuring your assets — through wills, trusts, gifting strategies, and beneficiary designations — so your wealth transfers the way you intend, with minimal tax drag. In 2026, with potential changes to estate tax exemptions, this planning is urgent.

What should I look for in a wealth manager for HNW planning?

Look for a CFP® or CPWA® who is a fiduciary, has a documented planning process, coordinates with your tax and legal advisors, and has clear protocols for identity verification and fraud protection. Ask for a written financial plan — not just an investment proposal.

How does retirement planning for high net worth individuals differ?

Retirement planning for high net worth individuals focuses less on “will I have enough?” and more on “how do I preserve, distribute, and transfer this efficiently?” Key issues include Roth conversion strategy, required minimum distributions, Social Security optimization, and multi-decade drawdown planning.

How does Percepture help wealth managers with HNW marketing?

Percepture builds AI-search authority for wealth managers through Enterprise SEO, Generative Engine Optimization (GEO), and Digital PR. The goal: when HNW prospects search — on Google or in ChatGPT — your name is the trusted answer.

Want HNW clients to trust you before the first call?

That is what digital PR + SEO + Paid targeting+ AI-search structure is built to do.

Connect with us today!

About Sid Bindra

Sid Bindra is a CFP® and founder of The Bindra Group, affiliated with LPL/Linsco. He was named to the Forbes Top Next-Gen Wealth Advisors Best-In-State list and has been recognized for his work with HNW families navigating complex financial transitions. Sid Bindra CFP® brings a preservation-first philosophy to high net worth financial planning — built on fiduciary accountability, disciplined process, and long-term client relationships. His $300M AUM move to Linsco was covered by Pulse 2.0 as one of the notable advisor transitions of the year.

Recommended Reading

- The Wealth Management SEO Company Built for Google and AI Search in 2026

- Why: Perfect for readers looking for the technical “how-to” of appearing in both traditional search and newer AI platforms like Perplexity.

- Generative AI in Wealth Management: Compliance, Deepfakes, and the “Department of Ethics”

- Why: Essential for addressing the “elephant in the room”—security and regulatory concerns that every RIA or financial firm is currently worried about.

- Wealth Management Marketing Agency in 2026: The Trust-First Growth System

- Why: Focuses on the “Trust-First” philosophy, which is the cornerstone of any successful long-term client relationship in the financial sector.