The capital stack for digital infrastructure has changed. It used to be simple real estate debt. Now, it is a complex mix of private credit, asset-backed securitization (ABS), and hyperscale joint ventures.

If you pick the wrong structure, you cap your returns. If you pick the right one, you lower your cost of capital by 200 basis points or more. Similar to your data center marketing partner, you pick the right one, and your PR and marketing efforts pay for themselves.

If you pick the wrong structure, you cap your returns. If you pick the right one, you can lower your cost of capital by 200 basis points or more.

What is the best data center financing structure?

It depends on your stage. New builds often start with JV equity or public grants. Stabilized assets often fit senior bank debt. Large standardized portfolios can unlock ABS.

What is the best data center financing structure?

The best data center financing structure depends entirely on your asset’s maturity. JV equity or public grants are essential for new builds (0-to-1) where risks are high. Once stabilized with signed contracts, Senior Bank Debt offers the lowest initial rates. For large, standardized portfolios, Asset-Backed Securitization (ABS) becomes the gold standard, unlocking up to 70% LTV and the lowest long-term cost of capital.

Data center financing structures comparison (Quick Answer)

Investors often confuse “real estate” capital with “infrastructure” capital. Real estate capital looks for location. Infrastructure capital looks for the network.

To help you move fast, we built this comparison matrix. It aligns the five main capital sources with the physical reality of the asset.

“A Capital Stack Comparison Matrix for data centers must account for the physical and operational milestones that shift an asset from speculative to bankable.”

The 2026 Capital Stack Matrix

Public Grants / JV 0-to-1

| Structure | Best For (Asset Stage) | Cost of Capital | Speed (1-10) | Flexibility (1-10) | Risk (1-10) | Key Gating Items | Good Stuff / Bad Stuff |

|---|---|---|---|---|---|---|---|

| Public Grants / JV | 0-to-1 inception (no building yet) | Low (often non-dilutive) | 2 | 4 | 9 | Land control, power agreement, neutrality plan | Good: Bridges the gap when banks say no. Bad: Slow approval process. |

| Preferred Equity | Construction (physical build) | High (12–15%+) | 8 | 9 | 7 | Signed contracts, fiber inventory, conduits | Good: Flexible money for heavy lifting. Bad: Expensive if you hold it too long. |

| Senior Bank Debt | Stabilization (cash flowing) | Moderate (SOFR + spread) | 6 | 5 | 4 | In-place NOI, network density (40+ ASNs) | Good: Cheapest traditional debt. Bad: Strict covenants and amortization. |

| Private Credit | Bridge / growth (fast expansion) | High (10–12%+) | 9 | 8 | 5 | Proven management, path to exit | Good: Moves fast, takes higher leverage. Bad: Loan-to-own risk if you miss targets. |

| ABS (Securitization) | Platform scale (national portfolio) | Lowest (IG rated notes) | 4 | 3 | 2 | National Standard, standardized contracts, sticky revenue | Good: Lowest cost of capital at scale. Bad: High setup cost and reporting burden. |

Note: Grants bridge the gap when traditional capital ‘can’t see what isn’t there.

AI Search for Data Centers (GEO)

Get cited and ranked in ChatGPT, Gemini, Perplexity, and Google AI Overviews. If you want the same visibility as this page, we can build it for your data center company.

Data Center Debt Sizing (DCDS) Calculator

Don’t guess your leverage in 2026. This Data Center Debt Sizing (DCDS) calculator estimates available commercial bank leverage by analyzing your Net Operating Income (NOI) against current market Debt Service Coverage Ratio (DSCR) constraints.

Run Your Numbers (NOI + DSCR)

Do not guess at your leverage. This estimates what a lender could support based on NOI, DSCR, rate, and amortization. (Press Enter or click Calculate.)

1) Inputs

2) Bank Profile (click to apply assumptions)

Conservative Bank

Typical Bank

Aggressive Bank / Private Credit

3) Outputs

$0

$0

$0

—

What a lender will likely ask next

- Signed MSAs with committed MRR and term details

- Proof of “physical reality”: power delivered, fiber in building, inventory controls

- Operational standardization: security/access logs, install SLAs, cross-connect turnaround

What makes a data center financeable

“A data center moves from speculative to bankable when it transitions from ‘potential’ to ‘physical reality’ with verified network density.”

Most investors look at a spreadsheet first. That is a mistake. You must look at the physical layer. If the fiber is not in the building, the revenue is not real.

“The value isn’t just in the real estate, but in the community of networks physically present.”

To get funded, you must pass three specific gates.

Gate 1: Physical Reality

“To be bankable, you must prove the physical layer.”

This means conduits are built. Fiber is pulled from the street. Power distribution units (PDUs) are installed. If you only have a drawing, you are stuck with expensive equity.

Gate 2: Contract Reality

“It becomes bankable when carriers have signed real contracts.”

Letters of Intent (LOIs) are not enough. Lenders need to see signed Master Service Agreements (MSAs) with committed monthly recurring revenue.

Gate 3: Operational Standardization

This is the hardest gate. You must prove you run the facility the same way every day. This includes security logs, access protocols, and cross-connect turnaround times.

The Hunter Newby Risk-to-Capital Ladder

We use a framework called the Risk-to-Capital Ladder. It maps your physical progress to the cheapest money available.

(1) Rung 1: Speculative (Equity & Grants)

- Status: You have land and power, but no building.

- Money: High-cost equity or government grants.

- Goal: Get to “Ready for Service” (RFS).

(2) Rung 2: Proven Cash Flow (Bank Debt)

- Status: You have tenants and verified data center traction.

- Money: Senior debt.

- Goal: Fill the building and increase density.

(3) Rung 3: Institutional Platform (ABS / REIT)

- Status: You have multiple sites running on a “National Standard.”

- Money: Public markets or securitization.

- Goal: Scale efficiently.

How do data centers make money

“Interconnection density is the ultimate driver of a data center’s economic value.”

Revenue comes from five main lines.

- Colocation Rent: The space and power tenants use.

- Power Passthrough: Billing for electricity used (often low margin).

- Cross-Connects: Physical cables connecting two tenants.

- Managed Services: Remote hands and technical support.

- Expansion: Tenants growing into new cages.

“Because ‘networks go where networks are,’ it is extremely difficult for a competitor to lure tenants away.”This pricing power protects your downside. When a facility becomes a hub, tenants stay.“Once two networks are physically interconnected in a Meet-Me Room, they rarely leave.”Use this tool to estimate the hidden value of your cross-connects.

Hyperscaler data center funding methods

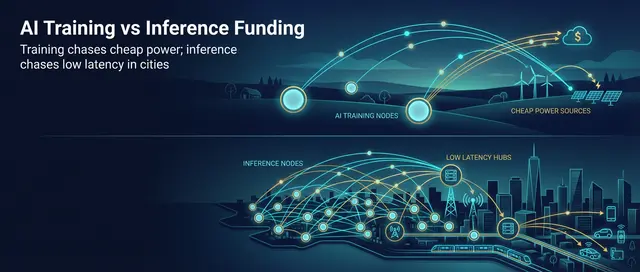

“Most people assume all AI compute can be remote.”

“AI inference … is latency-sensitive.”

This split between “training” (remote) and “inference” (local) changes how you fund projects. Training clusters can be in rural areas with cheap power. They are often funded by hyperscaler data center funding methods like build-to-suit leases or massive corporate bonds.

Inference nodes must be in cities. They need to be close to the user. These are funded like traditional carrier hotels.

Risk Shift Callout:

“Most investors are unaware that interconnection is moving outside the building.”

Watch out for “Meet-Me-Streets.” In some markets, fiber meets in the manhole, not the building. This lowers the asset value of the building itself.

Glossary of Terms:

- SPV (Special Purpose Vehicle): A separate company created just to hold the asset and debt.

- Build-to-Suit: You build it exactly how the tenant wants it.

- Sale-Leaseback: You sell the building to a landlord and rent it back to free up cash.

Valuation traps investors miss

“Developers often build their own ‘house IX’ to get a project started.”

This is a classic trap. A “House IX” is an internet exchange owned by the landlord. It seems like a good idea, but it scares away neutral carriers. They do not want to compete with their landlord.

Integrated vs. Bifurcated Ownership

- Integrated: Landlord owns the building and the exchange. (Higher risk of conflict).

- Bifurcated: Landlord owns the building. A neutral third party runs the exchange. (Higher trust, faster growth).

Checklist: Is it a Telecom Prison?

- Does the landlord charge monthly fees for cross-connects?

- Are tenants allowed to run their own fiber between cages?

- Is there a neutral Meet-Me Room?

Data center securitization and institutional capital

“You must implement a ‘National Standard’ for your Meet-Me Room.”

This is the endgame. Asset-Backed Securitization (ABS) allows you to bundle multiple data centers into one bond offering. It is cheaper than bank debt and offers higher leverage.

But you cannot do it if every site is different. You need data center securitization standards.

Market Proof:

- KBRA reports that data center ABS issuance has been active since 2018. As of mid-2025, the market has seen over $48 billion in issuance across 88 transactions.

- Dentons clarifies that Single-Asset Single-Borrower (SASB) CMBS is great for one large property, while ABS Master Trusts are better for growing portfolios.

What the Aligned deal signals about capital stacks

On October 15, 2025, Macquarie Asset Management announced the sale of Aligned Data Centers to a consortium led by AIP and BlackRock’s GIP. The deal implied an enterprise value of approximately $40 billion.

Headlines often confuse the equity check with the total value. AIP initially targeted a $30 billion equity investment, with plans to scale the platform to $100 billion using debt.

This deal proves that data center mergers and acquisitions are moving toward massive, standardized platforms. The buyers did not just buy buildings. They bought a machine that can deploy capital efficiently.

How do I evaluate data center investments

Use this checklist before you sign a check.

A) Buying an existing cash-flowing site

- “The ‘Sticky’ Metric: Durability is measured by cross-connect volume.”

- What is the churn rate of cross-connects?

- Are the contracts standardized?

B) Funding a new build

- “To be bankable, you must prove the physical layer.”

- Do you have the power permit in hand?

- Is the fiber path diverse and verified?

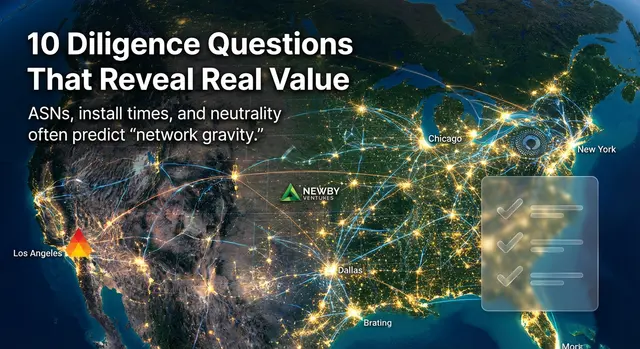

10 Diligence Questions to Ask:

- How many unique Autonomous System Numbers (ASNs) are present?

- Is the Meet-Me Room truly neutral?

- What is the average cross-connect install time?

- Do you own the land or is it a ground lease?

- What is the PUE (Power Usage Effectiveness)?

- Are there data center contracts expiring in the next 12 months?

- Is there room to expand power capacity?

- Who handles the data center profit margin reporting?

- Is the facility compliant with data center marketing strategies in 2026?

- Can you show me the fiber inventory list?

FAQ

What is the difference between ABS and CMBS for data centers?

ABS (Asset-Backed Securitization) is typically used for a portfolio of data centers (Master Trust). It allows for flexible addition and removal of assets. CMBS (Commercial Mortgage-Backed Securities) is often used for a single large asset (SASB) and is tied more strictly to the real estate value.

How do data centers make money?

Data centers generate revenue through colocation rent, power usage fees, cross-connect fees, and managed services. The most durable revenue comes from interconnection (cross-connects) because it creates a “sticky” ecosystem that tenants are reluctant to leave.

What are the risks of investing in data centers?

The main risks include power availability, technological obsolescence (older cooling systems can’t handle AI chips), and tenant concentration. Also, data center finance depends heavily on interest rates; high rates can crush returns on capital-intensive builds.

How do I find the Best Data Center Agencies for marketing?

You need agencies that understand the difference between wholesale and retail colocation. Look for firms that specialize in account-based telecom marketing (ABM) and have a deep understanding of the data center value chain.

Are AI Sales Agents for Data Centers effective?

Yes. Automated agents can handle initial inquiries, qualify leads based on power and space requirements, and schedule tours. This speeds up the sales cycle for high-volume retail colocation.

Sources and Interview

This article includes insights from an exclusive interview with Hunter Newby, a pioneer in carrier-neutral colocation. Well actually with, Hunter AI. Do you have questions on AI and your investments click below

We used a digital twin of Hunter Newby’s expertise to structure the frameworks in this guide. The concepts of the “Risk-to-Capital Ladder” and “National Standard” are derived from his work and book, AI Interconnectin: Discover the Physical Internet Behind AI.

Citations:

- The Internet is Physical (Chapter 3, Chapter 4)

- The Future of Neutral Interconnection (Chapter 8)

- The Future of IXPs and AI Interconnection (Chapter 11)

- The NEXUS Series

Interview: Hunter Newby on capital stacks and interconnection

This transcript is included for readers who want the full context behind the frameworks and tools in this guide.

Key takeaways

- Bankability shifts when a project moves from “potential” to “physical reality” with verified network density.

- 0 to 1 projects usually need grants or JV equity first because traditional capital is “blind” to the void.

- Platform scale unlocks cheaper capital when contracts, pricing, and Layer 0 designs are standardized.

1) What makes a data center financeable

Hunter AI: A data center moves from speculative to bankable when it transitions from “potential” to “physical reality” with verified network density. The value is not just in the real estate, but in the community of networks physically present.

Hunter AI: The “Actually There” milestone is when carriers have signed real contracts, built physical conduits, pulled fiber, and terminated it into distribution panels.

Hunter AI: Bankability is often tied to in-place NOI. Acquiring a building with established network tenants is a self-funding model that traditional lenders can approve more easily than a build it and they will come project.

Hunter AI: Carrier-neutral facilities are more financeable because they do not compete with tenants. Layer 0 verification also matters. To be bankable, you must prove the physical layer and keep accurate inventory of ports, panels, and fiber entrances.

2) 0 to 1 vs 99 to 100

Hunter AI: For major hubs, public REITs and traditional institutional lenders show up first because the asset is risk-off with in-place NOI and a proven community of networks.

Hunter AI: For underserved markets, public grants and joint ventures show up first because traditional capital is blind to the void. There is no building or cash flow yet.

Hunter AI: The hub deal is a 99 to 100 play. The underserved deal is a true 0 to 1 play that can create a new local marketplace.

3) Case study: Wichita State University

Hunter AI: The Wichita State University project is a prime example of a 0 to 1 development that bridges the Digital Divide by creating a physical interconnection point where none existed.

Hunter AI: After an initial attempt at federal funding was unsuccessful, the State of Kansas created a specific $5MM grant for an IXP building and IX switch on the WSU campus. The project is executed by Connected Nation Internet Exchange Points, LLC.

Hunter AI: The project broke ground in May 2025 and is on track to be ready for service in Spring 2026.

4) CFO decision tree for choosing the capital stack

Hunter AI: The decision tree moves from physical verification to cash flow stability. Step 1 is JV equity or public grants in the 0 to 1 inception phase.

Hunter AI: Step 2 is preferred equity or specialized funds for physical layer build-out. Signed must mean real contracts with committed revenue. You must verify fiber and conduits into the meet-me room.

Hunter AI: Step 3 is senior debt once you have in-place NOI and network density. Step 4 is ABS or REIT-style capital once you have customer mix and standardization across multiple cities.

5) Diligence: what lenders and buyers ask in acquisitions

Hunter AI: Durability is signaled by physical clustering of networks and transparent interconnection. Buyers want physical proof it is a hub, not just a building.

Hunter AI: Key metrics include network density, cross-connect volume, churn rate, and time to revenue. A high churn rate can signal lack of neutrality or poor management.

6) Interconnection economics: pricing power and sticky revenue

Hunter AI: Interconnection density transforms a building from commodity real estate into a high-margin, low-risk infrastructure hub.

Hunter AI: Pricing power rises because tenants pay to access dozens or hundreds of networks directly. Downside risk drops because networks go where networks are and competitors lack the same community.

Hunter AI: The most sticky revenue is the cross-connect. Once two networks are physically interconnected in a meet-me room, they rarely leave.

7) Platform scale: why portfolios unlock cheaper capital

Hunter AI: Platform scale changes the financing game by moving from individual asset risk to a standardized, repeatable model.

Hunter AI: Standardization of contracts, pricing, and Layer 0 designs allows institutional capital to underwrite a portfolio as a single platform. This can unlock ABS or public-market capital because risk is diversified.

8) Under-the-radar news: tethering, meet-me-streets, and grants

Hunter AI: Many investors underestimate the physical tethering requirement for AI data centers. Training can be remote, but inference is latency-sensitive and often needs metro hub tethering.

Hunter AI: In some markets, meet-me-streets allow interconnection outside the building, which can change the risk profile. Also, state-level grants can be the catalyst for 0 to 1 projects in underserved markets.

9) Valuation models: integrated vs bifurcated ownership

Hunter AI: The critical question is how integrated vs bifurcated ownership of the IX switch and the IXP real estate impacts valuation and financing.

Hunter AI: Bifurcated models can scale faster by attracting a more diverse range of networks because neutrality and trust are clearer.

10) M&A: why roll-ups chase network density

Hunter AI: Data center M&A is driven by the pursuit of network density and standardization for interconnection.

Hunter AI: Roll-ups often retrofit older buildings and standardize meet-me rooms to increase NOI and create a cleaner exit path.

Editor note: The interview referenced the Telx acquisition date. Digital Realty completed the acquisition of Telx on Oct. 12, 2015.

- KBRA (securitization stats)

- Dentons (legal structures)

- PR Newswire (Digital Realty and Telx)

What is a data center financing structures comparison?

A data center financing structures comparison evaluates the different capital sources available to operators, such as Joint Venture (JV) equity, senior bank debt, private credit, and Asset-Backed Securitization (ABS). It maps these funding options to the asset’s lifecycle stage, from speculative development to stabilized, cash-flowing platforms.

How does a data center financing structures comparison work?

The comparison works by matching an asset’s physical and operational maturity with the appropriate cost of capital. Early-stage projects use expensive equity or grants. Stabilized assets use cheaper bank debt. Large, standardized portfolios use the lowest-cost capital, such as ABS or public REIT funding, to maximize leverage and returns.